》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM metals

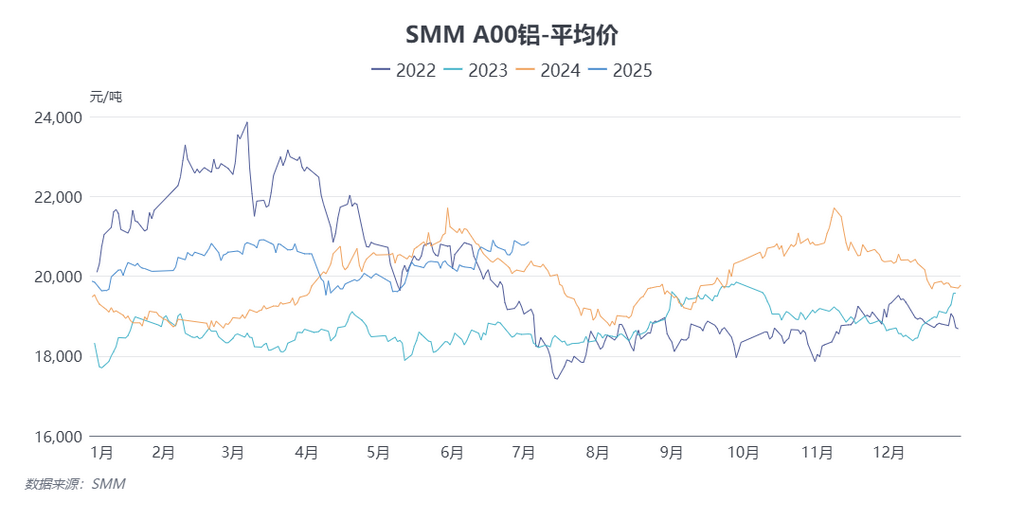

SMM News on July 3:

PV aluminum extrusion: This week, some leading PV frame extrusion enterprises in east China, southwest China, and Hebei reported that orders remained relatively saturated in the first week of July. Orders on hand provided certain support for the operating rate, and the operating rate of a few manufacturers increased slightly WoW. However, relevant enterprises reported significant uncertainty in subsequent orders, and there was still a risk of production cuts at module factories. It is expected that the operating rate will weaken in mid-July.

Raw material prices: During the period (June 30, 2025 - July 3, 2025), the center of the weekly average price of spot aluminum moved upward. The SMM A00 weekly average price was 20,807.5 yuan/mt, up 1.09% from the previous weekly average price. Overall, on the macro side, domestic economic data in June performed well. In response to the decline in consumer sentiment, favorable policies continued to be strengthened, and the direction of promoting consumption remained unchanged. Uncertainty in overseas macroeconomic games intensified, with the tariff deadline approaching on July 9, and market risk aversion sentiment grew stronger. On the fundamental side, casting ingot production increased at some aluminum smelters in certain regions. As July began, the off-season atmosphere was strong across downstream sectors. Coupled with the high aluminum prices further suppressing operating performance, spot market transactions were not ideal. Aluminum ingot inventory continued to build up, and spot premiums/discounts weakened significantly. The real-time cost of aluminum continued to decline MoM. Overall, the current low inventory still provides support for aluminum prices. However, under the triple pressures of inventory buildup expectations, weakening consumption, and macroeconomic uncertainty, it is expected that the risk of high aluminum prices facing downward pressure in the short term will intensify. There is still upside potential, but it is relatively narrow. Subsequent attention should be paid to casting ingot production and inventory changes. SMM expects that the most-traded SHFE aluminum 2508 contract will trade within the range of 20,300-21,000 yuan/mt next week, and LME aluminum will trade within the range of $2,550-$2,660/mt.

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)